|

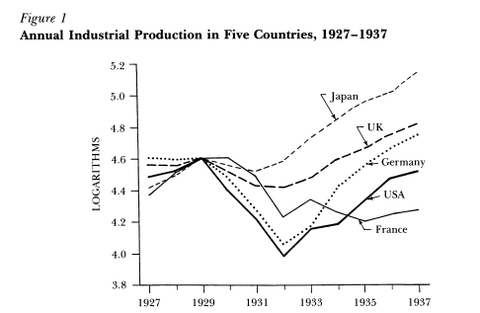

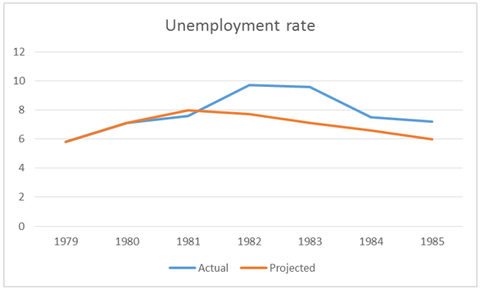

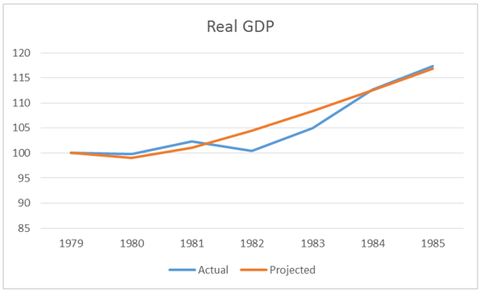

Il Nobel Krugman ha pubblicato recentemente sul suo blog due articoli, che come al solito sono sintetici ma allo stesso tempo molto chiari. Nel primo articolo evidenzia la somiglianza fra l'euro e il gold standard, sistema corresponsabile della grande depressione degli anni 30. In particolare sottolinea come una crisi di bilancia dei pagamenti, che è alla base degli squilibri interni alla zona euro, ci sia stata anche negli anni 30 (fra il 1919 e il 1933), con ingenti afflussi di capitali verso l'Austria, l'Ungheria e la Germania, che poi si sono improvvisamente arrestati e quindi sono "fuggiti" da questi paesi, con conseguenze disastrose. Infatti Krugman scrive : "...I knew that it was best viewed as a balance-of-payments crisis, not a debt crisis — a case in which large capital inflows to Europe’s periphery suddenly went into reverse. What I didn’t know was that something quite similar happened in Europe from 1919 to 1933, with huge inflows to Austria, Hungary and Germany suddenly shifting to huge outflows, and with similarly disastrous results..." Proseguendo nel suo discorso il professor Krugman ci fa notare che a seguito di un "Sudden Stop" (termine coniato da Calvo dopo la crisi Asiatica del 1990), con conseguente crisi economica, solitamente come una Fenice che rinasce dalle sue ceneri, arriva una ripresa ruggente. A conferma di quanto detto Krugman fornisce questo grafico sulla produzione industriale (1927 - 1937) in cinque paesi diversi :  Quello che Krugman sottolinea è il pessimo risultato della Francia dove non arriva la Fenice della rinascita economica, e si chiede perché la Francia è diversa? Semplice, perché è rimasta nel gold Standard. E da qui l'analogia con la crisi dell'eurozona, dove nonostante la profonda crisi che va avanti e peggiora da oltre 5 anni, non si intravede nessuna Fenice della rinascita, per un motivo molto semplice, L'EURO, che agisce in maniera simile al gold standard se non peggiore. Ecco le parole usate dal buon Krugman : "...Why was France different? It stayed on the gold standard. And it’s hard to avoid the notion that the absence of any phoenixes in Europe today comes from the role of the euro, which is acting as a similar constraint, only worse..". E conclude facendoci notare il "successone" dell'euro : "...But hey, Europe has just had one quarter of (modest) growth. The euro is a triumph!" Nel su secondo articolo o professor Krugman viene analizzato l'evidente fallimento dell'austerità dal punto di vista economico, che però rischia di diventare un successo dal punto di vista politico. Nel sottolineare che l'austerità ha fallito a tutti i livelli per i seguenti motivi : 1 - fra fine 2012 e inizio 2013 nonostante debiti e deficit pubblici siano cresciuti in tutto il mondo, Europa compresa, i tassi di interesse sono rimasti bassi; 2 - a seguito dei moltiplicatori che il FMI ha ammesso essere superiori ad 1, in recessione tagliare la spesa e aumentare le tasse è distruttivo per l'economia; 3 - il presunto limite del 90% del rapporto Debito Pubblico/PIL oltre il quale la crescita rallenta bruscamente, non esiste; il professore ci fa notare che nulla è cambiato nelle politiche economiche di austerità per due motivi : 1 - a lungo andare le economie tendono a migliorare anche a seguito di crisi causate da pessime politiche economiche; 2 - la gente tende a dimenticare gli eventi più lontani nel tempo e a ricordare solo quelli più recenti. Quindi fondamentalmente gli austerians non devono far altro che aspettare, perché primo o poi la ripresa arriva e possono prendersene il merito, ecco le parole esatte di Krugman : "...Over the course of fall 2012 and spring 2013, the opponents of austerity were vindicated on every intellectual front. Interest rates stayed low despite high debt and deficits (and fell in Europe once the central bank began doing its job as lender of last resort). The evidence became overwhelming that cutting spending and raising taxes in a slump depressed output, and by much more than the IMF had previously assumed. The alleged debt cliff, with growth falling off sharply once debt exceeded 90 percent of GDP, turned out not to exist — and even the mild negative correlation between debt and growth seems to be mainly reverse causation. But nothing changed in policy — and the austerians may well come out as political winners despite having been wrong about everything. Why? Well, there are two facts you need to know. One is that economies tend to improve, eventually, even if they’ve been depressed by bad policies. The other is that voters, and to an important extent the chattering classes as well, evaluate politicians not by the absolute level of income, far less by a comparison between how things are with how they should be, but by the recent rate of change. So in an important sense all the austerians had to do was hang on long enough. Sooner or later there would be an upturn, and they could claim credit..." A conferma di quanto scritto, Krugman porta l'esempio del presunto successo della Reganomics degli anni 80, mostrandoci due grafici dove sono riportate le previsioni fatte dal Congressional Budget Office (CBO) prima dell'elezione di Regan, sulla Disoccupazione (fig 1) e sulla crescita reale del PIL (fig 2), ecco i risultati :   Come si vede chiaramente le previsioni (soprattutto sulla disoccupazione) sono diversa dai dati reali, e come suggerisce Krugman l'unico dato migliore del previsto è quello sull'Inflazione, che il CBO aveva previsto all'8% e che in realtà è stata sotto il 4%, ma per questo non c'è da stupirsi visto l'alta disoccupazione e la curva di Philips.

Il riassunto di Krugman è : "...So a quick summary of what happened during Reagan’s first term is that the U.S. economy experienced a much worse slump than almost anyone expected, then recovered by 1985 roughly to trend, with unemployment still somewhat elevated. On the whole, it was a bad record, with hundreds of billions of potential output wasted and a lot of gratuitous pain for the unemployed. But that, of course, is not how it played politically. Because output was growing fast and unemployment falling fast in 1984, as the election approached, it was Morning in America! Supply-side economics vindicated, Keynesianism destroyed! And this legend lives on to this day..." Capito, il primo mandato di Regan è stato un fiasco, ma con l'avvicinarsi delle elezioni per il secondo mandato, è arrivata la ripresa che ha consacrato il liberismo e l'austerità e ucciso il Keynesismo. La conclusione è che qualcosa del genere possa succedere anche in Europa : "...I think we need to face the possibility that something like this may happen in the UK, and maybe even in Europe. But even if it does, the answer is to keep on plugging away at the truth, and remember that the wheel of fortune turns. Remember, it was only 8 years from Morning in America to “It’s the economy, stupid.” Dal blog del Nobel per l'economia Paul Krugman : But Where’s My Phoenix? e When Good Things Happen to Bad Idea Addendum del 18/09/2013 A conferma della rivendicazione di vittoria da parte dei difensori dell'Austerità, arriva questo articolo del Telegraph a firma di Evans-Pitchard, che riporta le parole del ministro tedesco Schauble, che sta già rivendicando i presunti benefici che sta portando il consolidamento fiscale via austerità, visto che la zona euro nel secondo trimestre 2013 è cresciuta dello 0,3%. Dal Telegraph : My grovelling apology to Herr Schäuble Buona informazione a tutti.

0 Comments

Leave a Reply. |